June 9, 2026

What Nobody Tells You About High-Earner Taxes: A 101 Guide to Stock Options and Executive Compensation

When you receive stock options, Restricted Stock Units (RSUs), or equity-based executive compensation, it feels like a massive financial win. However, without a strategic plan, a significant portion of that wealth can easily be lost to high tax brackets or market volatility. Managing tech equity requires moving beyond basic budgeting and learning how to shelter your income, optimize your tax filing, and protect your hard-earned gains.

What Is Executive Compensation Equity, and How Is It Taxed?

Direct Answer: Executive compensation equity refers to non-cash benefits like RSUs, Incentive Stock Options (ISOs), and Non-Qualified Stock Options (NSOs) granted to high-performing employees and tech professionals. Each type of equity triggers vastly different tax events—ranging from ordinary income tax upon vesting to capital gains tax upon sale—making strategic timing essential to avoiding massive tax bills.

When you are awarded equity, the IRS views it differently depending on how the asset is structured. For instance, RSUs are generally taxed as ordinary income the moment they vest, based on their fair market value. Stock options, on the other hand, grant you the right to buy shares at a set price, meaning you control the exact timing of your tax liability.

Navigating the ISO vs. NSO Tax Traps

- Incentive Stock Options (ISOs): These offer distinct tax advantages because you don't owe ordinary income tax when you exercise them. However, they can trigger the dreaded Alternative Minimum Tax (AMT), which catches many tech professionals off guard.

- Non-Qualified Stock Options (NSOs): These are less tax-favored. The moment you exercise NSOs, the spread between your strike price and the market value is immediately taxed as ordinary income.

If you don't map out these triggers in advance, you might find yourself asset-rich but cash-poor when tax season arrives.

Featured course

Executive Compensation Equity and Taxes

A beginner-friendly guide to understanding and negotiating complex executive compensation packages. Learn how to optimize your tax strategy, avoid common financial traps, and balance immediate cash with long-term equity growth.

This course is designed for tech professionals who need to decode the exact tax mechanics of their equity packages, helping you maximize what you keep and minimize what you owe.

How Can High Earners Shield Equity Gains from High Tax Brackets?

Direct Answer: High earners can shield their equity gains from top-tier tax brackets by utilizing advanced IRS-approved mechanisms like Backdoor and Mega-Backdoor Roth strategies. These vehicles allow professionals to route post-tax income into retirement accounts where the investments can grow and be withdrawn entirely tax-free, bypassing standard income limits.

If your tech equity pushes your income into the highest U.S. tax brackets, standard retirement vehicles like a traditional 401(k) or a basic Roth IRA won't provide enough relief due to strict contribution limits. This is where advanced wealth-routing strategies become essential.

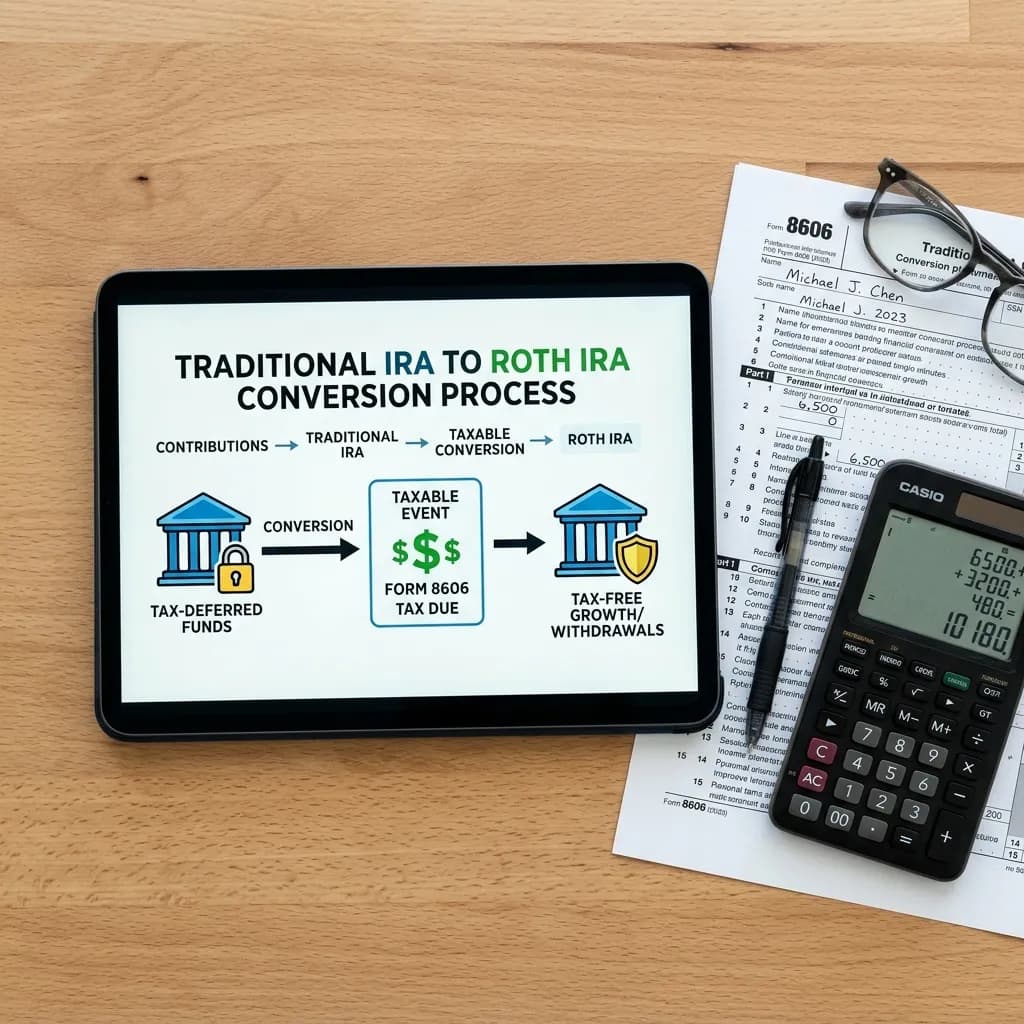

Maximizing the Backdoor Routing Ecosystem

- The Backdoor Roth IRA: By contributing post-tax money to a Traditional IRA and immediately converting it to a Roth IRA, you legally bypass the standard Roth income ceilings.

- The Mega-Backdoor Roth: If your employer's 401(k) plan allows after-tax contributions and in-service distributions, you can potentially roll over tens of thousands of additional dollars into a tax-free environment each year.

Implementing these maneuvers requires precise execution to avoid violating the IRS "pro-rata rule," but the long-term tax savings on your compounding equity investments are immense.

Featured course

Backdoor and Mega-Backdoor Roth Strategies

A practical guide for high earners to bypass income limits and maximize tax-free retirement growth. Learn the step-by-step execution of Backdoor and Mega-Backdoor Roth strategies while navigating complex tax rules to avoid common pitfalls.

Master the exact legal mechanics required to execute backdoor conversions smoothly, ensuring your high income doesn't block you from tax-free growth.

What Is the Best Way to Rebalance a Portfolio Without Triggering Massive Taxes?

Direct Answer: The most efficient way to rebalance a concentrated equity portfolio without triggering massive taxes is through systemic tax-loss harvesting and capital gains management. This process involves strategically selling underperforming assets to offset the capital gains realized from selling your highly appreciated tech stock, keeping your net tax liability as close to zero as possible.

Holding too much of your net worth in your company’s stock leaves you incredibly vulnerable to market downturns. Financial advisors universally recommend diversifying, but selling a massive block of vested tech stock all at once can trigger an overwhelming capital gains tax bill.

Rules for Strategic Gain Management

- Tax-Loss Harvesting: You can offset capital gains dollar-for-dollar by realizing losses on underperforming investments. If your losses exceed your gains, you can use up to $3,000 to offset ordinary income.

- The 30-Day Wash-Sale Rule: To claim a loss, you cannot buy the same or a "substantially identical" security within 30 days before or after the sale.

- Holding Timelines: Always differentiate between short-term capital gains (taxed at high ordinary income rates) and long-term capital gains (taxed at much lower rates of 0%, 15%, or 20%), holding assets for over a year whenever viable.

Featured course

Tax-Loss Harvesting and Gain Management

A practical guide to reducing tax liability by strategically offsetting capital gains with investment losses. Learn to navigate IRS rules, implement advanced direct indexing, and optimize asset location across different account types.

Learn how to systemically offset your equity wins with smart portfolio balancing techniques, keeping your diversification strategy completely tax-optimized.

Ready to Diversify Safely?

See how Dotwise breaks down complex topics like investing and tax optimization into 5-minute, scannable summaries you can read anywhere.

See how it works and sign upFrequently Asked Questions About Tech Equity and Taxes

What happens if my company stock drops after I exercise my ISOs?

If you exercise ISOs and the stock price plummets before the end of the calendar year, you could face a massive AMT bill based on a "phantom" value that no longer exists. If you sell the stock in the same calendar year you exercised it, it converts to a disqualifying disposition, which changes how it is taxed but can eliminate the AMT trap.

Can I use the Mega-Backdoor Roth strategy at any company?

No. To utilize the Mega-Backdoor Roth, your company's specific 401(k) plan must explicitly allow two features: after-tax contributions (which are distinct from standard pre-tax or Roth contributions) and in-service non-hardship distributions or roll-overs.

How do I avoid the Wash-Sale Rule when harvesting losses?

To avoid the wash-sale rule, you must ensure you do not purchase the same stock, or mutual funds and ETFs tracking the exact same index, within a 61-day window surrounding your sale. Instead, temporarily move those funds into an asset that behaves similarly but tracks a different index to maintain your market exposure.

Master Your Financial Blind Spots with Dotwise

Managing advanced wealth concepts means confronting a hard truth: you don't know what you don't know. Most personal finance books only cover mundane, entry-level budgeting topics because they have to appeal to the masses. They don't address the complex realities of tech equity, high tax optimization, or multi-tiered retirement strategies.

Dotwise solves this problem by mapping out all your financial blind spots in one place. Instead of spending days sifting through fragmented, unverified forum posts, Dotwise delivers highly curated, structured courses built directly from reputable, authoritative financial sources. Every article is densely cited so you can verify the underlying data instantly.

Because these are advanced materials, the courses are broken down into bite-sized chapters designed to be read over a few days in your spare time. Our flexible web application saves seamlessly to your mobile phone’s home screen, functioning just like a native app. Whether you have 5 minutes during a commute or on the couch before bed, Dotwise remembers your exact progress so you can pick up right where you left off yesterday.

Build Your Personal Wealth Roadmap Today

Sign up to get 5 articles per month completely free, or unlock our entire library of advanced financial courses for just $10.99/mo with a 7-day free trial.

View details and sign up today